MEP Watch: About Those Plans to Bail Out Union Pensions

by meep

I’m still working on the Illinois POB projections, so in the meantime, let me go to this thing that has been bubbling around with (primarily) Democratic Senators doing events… probably to claw back areas that had been lost to Trump in 2016.

It’s a plan to bail out multiemployer plans – well, some of them.

I wrote about this at the beginning of December, and the activity has continued. I’m not sure that this is necessarily going to grab attention from whatever Trumpery people are hyperventilating about (and I don’t know if Trump is ever going to weigh on on this), but I figure I should give an update of what’s been going on.

This is about the Butch Lewis Act, which supposedly is about providing loans to the failing plans… but… well, we’ll get to the detail later. (it’s a bailout)

NEWS ITEMS ON POSSIBLE MEP BAILOUTS

Here are all the news/editorial items I have grabbed since the December 7 post, talking about this bailout plan. Sorry if some of the links no longer work – I grab these items as they occur. You may be able to find some in the internet archive.

- Beacon Journal/Ohio.com editorial board: Congress and its duty to secure these pension benefits

- Don’t Make Taxpayers Bail Out Pension Plans

- Looming pension shortfalls to complicate next shutdown fight

- Miners’ Pensions A Major Part Of Spending Debate

- Liberal Lawmakers Trying to Bail Out Private Pensions With Taxpayer Money

- New York Republican Peter King Supports Pension Bill

- Minnesota’s New Senator Prepares to Fight for Teamsters Pensions

- Lawmakers Working to Overhaul Pension Rules

- The time is now to ensure multiemployer pension plan security

- ‘Pension Plans Face Looming Crisis,’ Rep. Marcy Kaptur Says

- Dean Baker: The Attack on Workers’ Retirement

- Smith meets with Teamsters: Minnesota’s new senator prepares for fight over pensions

- Senator Tina Smith Meets With Retirees About Pension Problem

- Will Congress break pension promise to coal miners, millions of other Americans?

- Schumer, King, Teamsters push for bill to cover pensions

- Teamsters, NY Congressmen Partner for Union Pension Bill

- Pension plans can’t be the next big taxpayer bailout in America

- U.S. Chamber of Commerce: Why You Should Care About the Multiemployer Pension Crisis, plus their white paper on the crisis

- Opinion: A million participants in multiemployer pension plans face a loss of benefits

- Sherrod Brown and Democrats have a plan to save pensions. Now Congress must decide if it’s a rescue or a bailout

- Democrats push to add pension fix to spending bill

- Lawmakers pushing legislation to save union pension funds

- Sen. Brown plans to bring Ohioan facing massive pension cut to Tuesday’s event

- Senate Minority Leader Chuck Schumer Announces Teamsters Pension Developments In Albany

- Sen. Charles Schumer Pitches Teamsters Pension Rescue Plan

- Sen. Heidi Heitkamp: Pension protections need to be in new spending bill

As I said, it’s bubbling along. I do want to mention that a few of these plans (such as the coal miners one) are in a special situation with regards to federal guarantees, I believe, but everything is trying to be lumped together… and not all MEPs are in awful shape.

For example, the pro sports MEPs seem to be doing pretty well, considering the facts of employment patterns for those participating in those plans. (Okay, the NBA plan still seems iffy to me.0

I hear tell the Senate has been getting close to some sort of bipartisan spending deal… I have no idea if the MEP bailout plan is part of that deal, or it’s just one chip that will get thrown away in favor of something else Democrats want more.

BASIC FACTS ON MEPS AND THEIR FAILURE

Some extremely basic facts:

- The U.S. government did not promise specific pension benefits to these people (not even Social Security… but the lack of SocSec promise is for everybody involved, not just MEP members)

- The promises, such as they were, were negotiated via the unions the participants are or were in

- The Feds kind of guarantee a minimum benefit for insolvent plans via the PBGC

- That guarantee for MEPs is extremely low

- A law was passed in the buttcrack of 2014 Congressional season, allowing for MEP benefits to be cut for participants and retirees before complete insolvency

- There are loads of requirements to fulfill to get these cuts, and the benefits given after the cuts have to be more than that minimum guaranteed amount

Here is some lovely research from the Society of Actuaries on MEPs. John Bury writes on some of it here (as well as other research reports.)

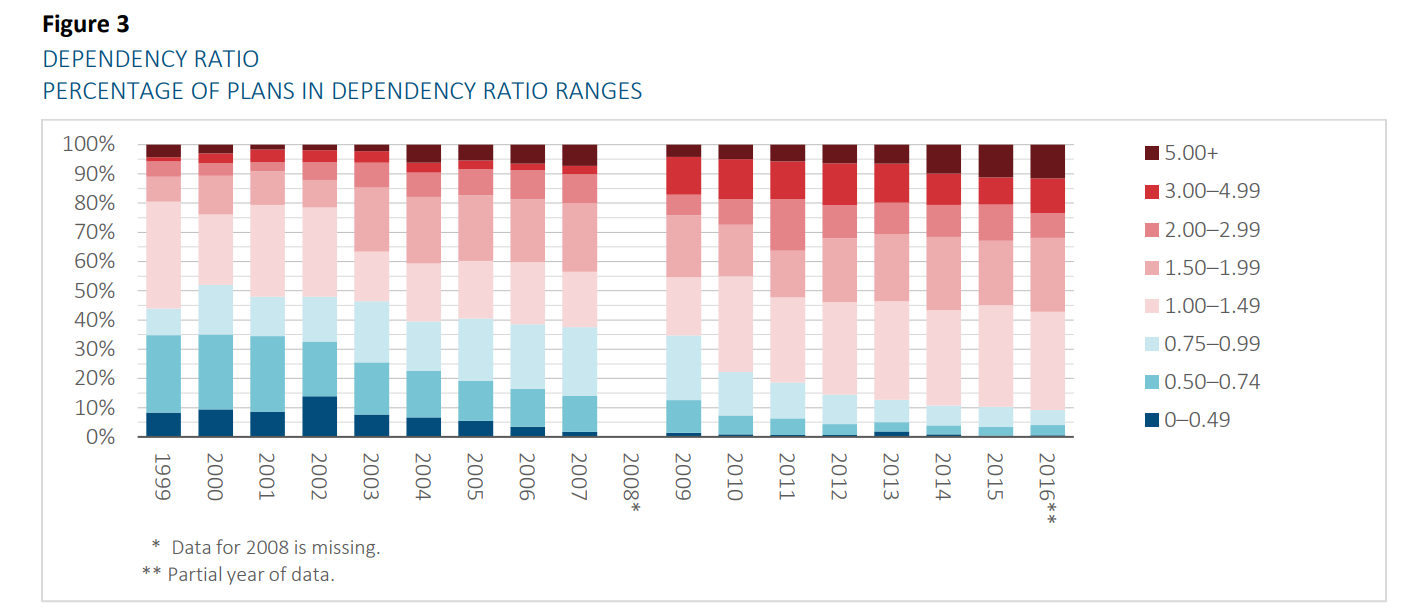

Let me grab a few graphs: first, though it’s at the end, is the dependency ratio. It’s just how many retirees/beneficiaries there are per active participant.

I believe these percentages are by count of plans, and not weighted by number of participants. (And lovely that the 2008 data are missing, but it’s not the fault of the researchers, I know.)

Here is the magic divide: blue (more active participants than retirees) vs. red (more retirees than active participants). Even in 1999, the ratios were not that hot looking. But yikes, in 2015, only 10% of plans had more active participants than retirees/beneficiaries.

IF the MEPs were fully-funded, with good risk management, yadda yadda, these dependency ratios would not be concerning.

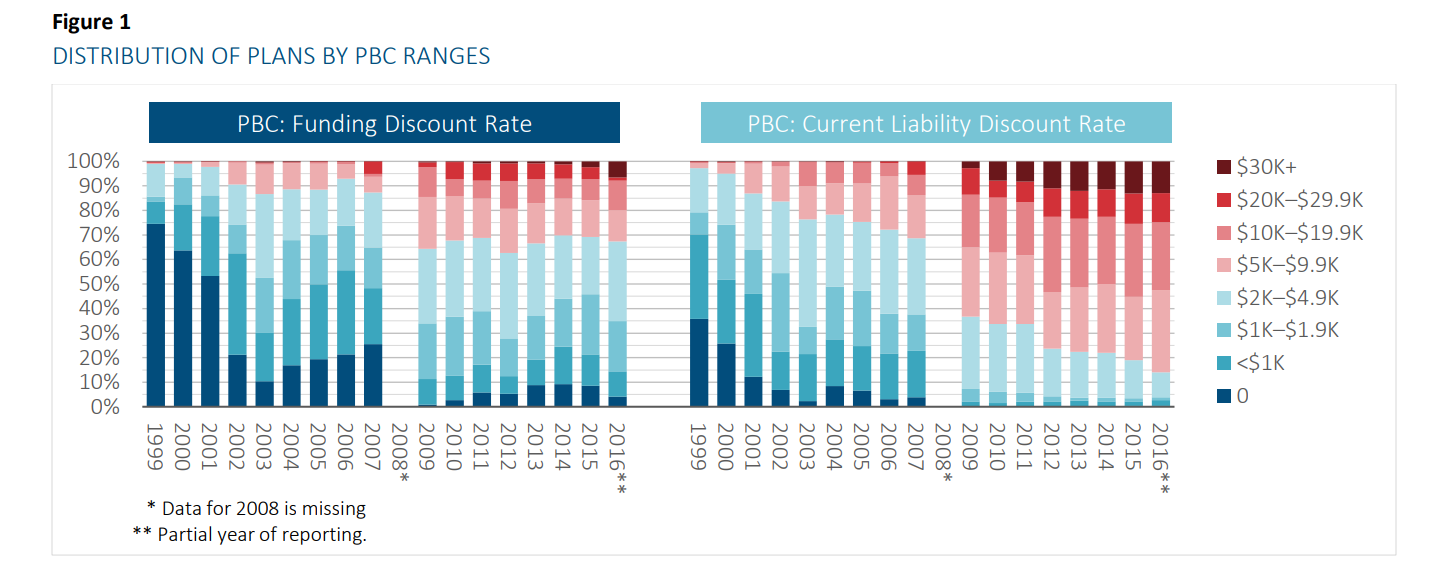

But… well, here’s the other graph I pulled:

The PBC refers to Previous Benefit Cost. Here is what the researchers say:

A plan’s PBC represents the annualized cost of funding its unfunded liability per active participant. The median PBC using funding discount rates was −$621 for 1999, indicating a small funding “surplus” rather than an unfunded liability. The median peaked at $3,799 for 2009 and has generally declined since to $2,119 for 2015. However, preliminary indications suggest an uptick for 2016. Unfunded liabilities for 2016 increased, most likely because of low investment returns during 2015.

I like that they provide two measures here, but that’s diving into actuarial details, and so that’s all I have to say about that.

HOW MANY MEPS HAVE APPLIED TO HAVE BENEFITS CUT?

As of right now, there are 21 entries in applications for MEP benefit suspensions, some of which are from the same MEPs reapplying.

Only four of these applications have been approved thus far, five were denied, three are currently in review, and the 9 remaining were withdrawn.

That’s not necessarily a lot of MEPs, though some of involved are huge. John Bury has been keeping good tabs on applications as they go through the process. He gives stats for each plan applying.

HERITAGE FOUNDATION WEIGHS IN: IT’S A BAILOUT

A nice long piece by the Heritage Foundation: Why Government Loans to Private Union Pensions Would Be Bailouts—and Could Cost Taxpayers More than Cash Bailouts

SUMMARY Less than one of every 500 workers and retirees who have union-run pensions belongs to a well-funded pension plan. To avoid workers bearing the consequences of irresponsible pension management by their employer and union trustees, plan advocates and some policymakers want taxpayers to bail out private-sector union pensions through highly subsidized government loans and other forms of assistance. Bailouts are never a good idea. They encourage more of the same type of mismanagement, negligence, and even corruption that contributed to the original problem. Bailing out pensions will only encourage businesses and unions to do more of the same—promising plush future pension benefits while failing to set aside the funds to pay for those promises.

KEY TAKEAWAYS

1. Private, union-run pensions are not too big to fail—but they are too expensive to bail out.

2. Government loans to insolvent pensions are bailouts, and bailouts reward the behavior that caused the financial problems—and encourage future irresponsibility.

3. A union pension would cost taxpayers more than $500 billion—and set the precedent for a $6 trillion taxpayer bailout of troubled state and local pension plans.

In fact, there’s more of an argument to bailout state and local pension plans more than MEPs.

The people in MEPs are covered by Social Security, and many people in the failing public plans are not. The MEP benefit guarantees from the PBGC may be low, but they’re not zero – public plans have no backstop.

When government goes out of business, some people can end up with nothing.

IS IT ACTUALLY A BAILOUT, THOUGH?

Here is what the Heritage paper says about the Butch Lewis Act:

Government Loans to Insolvent Pensions Are Bailouts

Government loans are often characterized as subsidies instead of bailouts because, by offering lower interest than available in the market, the loans encourage more of a particular activity—such as attending school or purchasing homes—than would otherwise occur. Subsidies represent the difference between what the market would charge for a loan versus what the government charges. Bailouts, on the other hand, essentially provide get-out-of-jail-free cards to negate the consequences of wrongful, reckless, or irresponsible actions.

Government loans to insolvent pension plans would be bailouts. Some of the plans that would qualify for loans would not qualify for any loan in the private market, and many would receive “junk” investment ratings at best. They certainly would not qualify for loans that offer interest-only payments for the first 15 or 30 years. Moreover, the purpose of the proposed government loans to insolvent pension plans is not to encourage more insolvent pension plans (although that is exactly what it would accomplish), but rather to try to remedy the damage done after decades of irresponsible and reckless pension-plan management.

This makes these loans a bailout—not a subsidy—and a particularly risky and costly bailout at that.

I agree they are a bailout, but it’s not just by giving them under-market interest rates to borrow at.

It’s this: the government absolutely has no recourse to claw back any money from the pensions. Many of these MEPs are in decline because the number of active participants (and participating employers) are declining in numbers, while the retirees are booming in number. As we saw from the SOA study above, that’s a widespread problem.

The only way these “loans” would get paid back is if there were future contributions to the MEPs that paid not only for new participants, but for unfunded liabilities already accrued. The plans with MPRA applications are not showing growth in new contributions – that’s a huge part of the problem.

Then there’s the whole fake arbitrage issue.

I think it would be better to outright sell this as a bailout – and some supporters are. Good for them. Pretending that the plans will actually pay back the loans is ludicrous — cash will be flowing out of the plans to provide benefits for the large number of retirees (compared to active participants), many of these industries will continue to dwindle, and that will be that. The government has no way to get the money back.

I can see this sort of bailout for declining blue collar industries appealing to Trump, even if it wouldn’t appeal to many coastal Democrats or conservative Republicans. I could see this being added to some sort of bipartisan deal….

…..but maybe it won’t be.

I do keep a watch on these stories at the Actuarial Outpost (with minimal commentary from me – it’s my external memory til I’m ready to blog), so you can follow that link if you want more timely updates than once every couple months.

I keep multiple news feeds on pension issues, and I’ve noticed the coverage of the MEP issue has been very focused in particular geographic areas or in very wonky political publications. This is not on a widespread publication like the tax bill. So I wouldn’t be surprised if nothing comes of the Butch Lewis Act. Now.

We’ve seen some of these bills put out by parties out of power before, as trial balloons, not only to garner electoral support (and fundraising) but also to work out kinks before the real legislation hits the President’s desk. It might be there more for a 2020 election issue than 2018.

But we’ll see.

Related Posts

Troubled Multiemployer Pensions: Central States Teamsters Files for Bailout

It's Happening: First Union Voted to Reduce Retiree Benefits

On the Bailouts That Didn't Happen, Part 1: Multiemployer Pensions