States and Cities under Fiscal Pressure: Bailouts, State Bankruptcy, and the Next COVID Bill

by meep

Well, it sounds like Senate Republicans finally woke up last week and decided to meet the HEROES battle coming from the House.

Senate GOP to unveil coronavirus relief plan next [this] week, McConnell says

Senate Republicans will delay the release of their coronavirus relief plan until next [this] week, Senate Majority Leader Mitch McConnell said Thursday [July 23], assuring Congress will miss a deadline to extend a key unemployment insurance boost.

“The [Trump] administration has requested additional time to review the fine details, but we will be laying down the proposal early next week,” the Kentucky Republican said. “We have an agreement in principle on the shape of the package.”

The GOP had hoped to unveil legislation as soon as Thursday, which would have kickstarted talks with Democrats on a bill that could pass both chambers of Congress. But Senate Republicans have not been able to nail down final details with the White House even as millions of jobless Americans move closer to a financial cliff.

States will stop paying out out the $600 per week enhanced unemployment benefit passed in March at the end of this week. The policy formally expires at the end of July.

Most of the talk for “retail” news has been on stuff like unemployment coverage, and other things focused on individuals. But states and cities are still cap-in-hand for a bailout.

Republicans, who want their bill to cost roughly $1 trillion, will need Democratic support to pass legislation in both the Senate and House. Democrats, who pushed a $3 trillion rescue package through the House in May, do not consider the GOP spending plans adequate.

They want rent and mortgage assistance as a federal moratorium on evictions is set to expire at the end of the week. Democrats have also pushed for a hazard pay increase for essential workers.

The party’s leaders have also pushed for more aid for cash-crunched state and local governments, which have warned they will have to cut back on employees or essential services due to the pandemic. The Republican proposal would not provide new money to states and municipalities but instead give them more flexibility in how to spend aid approved earlier this year, according to Mnuchin.

Aid approved earlier in the year is a lot less than what they hope to spend, don’t you think?

So let me run down the stories I’ve come across on potential bailouts, state bankruptcy, and more since my previous look at the issue, a month ago. Most will be in a biglonglist at the end of this post.

No, the “Blue” states aren’t “donating” their taxpayers’ money to other states’ residents

The point of this argument (and I link to a couple versions of it at the end of the post) is this: that NY has supposedly been shoveling its precious tax dollars into the federal maw, and getting a lot less out… so cough up now, everybody!

Op-ed in the WSJ: New York Is No ‘Donor State’

As the July 31 expiration date looms over the Cares Act’s unemployment bonus, all eyes will turn to the next — and, according to Senate Majority Leader Mitch McConnell, the last — coronavirus relief bill. Chief among Democrats’ priorities is a “blue-state bailout.”

They argue that high-tax states, which tend to vote Democratic, pay more in federal tax receipts than they get back, thereby subsidizing low-tax states, which tend to vote Republican. New York Gov. Andrew Cuomo keeps flogging a list of “donor states,” topped by New York, which “gave” $29 billion a year more than it “got” from 2015 through 2018.

Mr. Cuomo’s argument — that blue states like New York have lined federal coffers for years, so it’s only fair the feds return the favor — might be compelling if it were true. But the facts are sourced from a Rockefeller Institute report that miscounts what states receive. In truth, high-tax blue states are net “receivers” of federal funds, New York foremost among them.

The subsequent figures come from the Rockefeller Institute’s “Giving or Getting? New York’s Balance of Payments with the Federal Government” study, first published in 2017, with its most recent update in January 2020.

There are lots of problems with the Rockefeller Institute’s analysis.

Back to the op-ed:

It isn’t so simple. A food stamp isn’t the same as a serviceman’s paycheck. The former can reasonably be characterized as a federal subsidy — “a gift” in Mr. Cuomo’s parlance — while the latter cannot. The Rockefeller report treats both as gifts, distorting who gets what.

Texas is home to nearly 219,000 military personnel, New York 60,000. It’s no surprise federal defense-related expenditures in Texas dwarfed those in New York in 2018, $65 billion to $14 billion. From this the Rockefeller report implies Texas got $51 billion more than New York — for the privilege of defending the whole country.

….

The Rockefeller report also flatters the Empire State by leaving out the federal subsidization of municipal debt issuance. Washington lets states and localities issue debt that is tax-exempt at the federal level, thereby subsidizing each dollar of issuance. In 2018, New York issued $34 billion of long-term tax-exempt municipal debt; applying the Congressional Budget Office’s 2018 forward-looking estimate of 26 cents in federal subsidization per dollar of issuance implies roughly $9 billion in subsidies, increasing New York’s “take” in 2018 from $2 billion to $11 billion.High-tax, high-debt blue states dominate this market. The four biggest — California, New York, Illinois and New Jersey — issued almost $91 billion in tax-exempt munis in 2018, about a third of all issuance, collecting nearly $24 billion in federal subsidies. These states reap the benefits while exporting the costs to entrepreneurs, who have to pay more for scarcer capital. Rather than conducting diligence on a small business looking for capital, wealthy households have been absorbing municipal issuance. They own most of it.

This sounds about right. Yes, institutional investors such as insurers also invest in municipal bonds; said institutional investors often get less use out of the tax-free nature of muni bonds in general. And for iffy debtors like New Jersey and Illinois, the institutional investors generally think of capital requirements more. Which muni issuers have more retail investors differs.

Finally:

Finally, the Rockefeller report flatters high-tax states like New York, many of whose retirees migrate to low-tax states such as Florida, where they receive benefits. This allows New York to claim its residents pay an estimated $2 billion more in Social Security taxes than they receive in benefits. Logically, high-growth states with expanding working-age populations would register positive spreads on this metric. New York is neither while Florida is both. But the Sunshine State is saddled with a $21 billion negative spread, thanks to retiree flows. Neutralizing New York’s illusory $2 billion spread raises the state’s take from $11 billion to $13 billion.

More to the point — New York state doesn’t “own” either the FICA taken out of my wages or even the FIT. When (if) I get Medicare & Social Security later on, that will be due to me, not the states I lived and worked in at various times in my life.

It’s not Florida’s fault that people don’t find New York an amenable place to retire.

In any case, all of that goes back to indicate that most to the point, if anybody is to be compensated for being over-taxed, it should be me directly, not New York state.

And no, that doesn’t mean I’m softening re: SALT caps.

Only Fair State/Local Approach: Per Capita Federal Subsidy

If they really want to make a federal bailout of states and cities “fair”, the only true way to do this is to have the federal subsidy be based on the population of the state/city being given cash. It’s not the federal government’s business what level of taxes (and in what form) each state and local government decides to take out of its residents, visitors, and more.

They’ve already sent money to states and cities for use in fighting COVID. So it doesn’t even have to do with how hard-hit a state or city has been.

Of course, this is assuming any sort of additional funds are going to states and cities. And ignoring that the Federal Reserve set up a credit facility for states and municipalities, which Illinois has been the first to draw from.

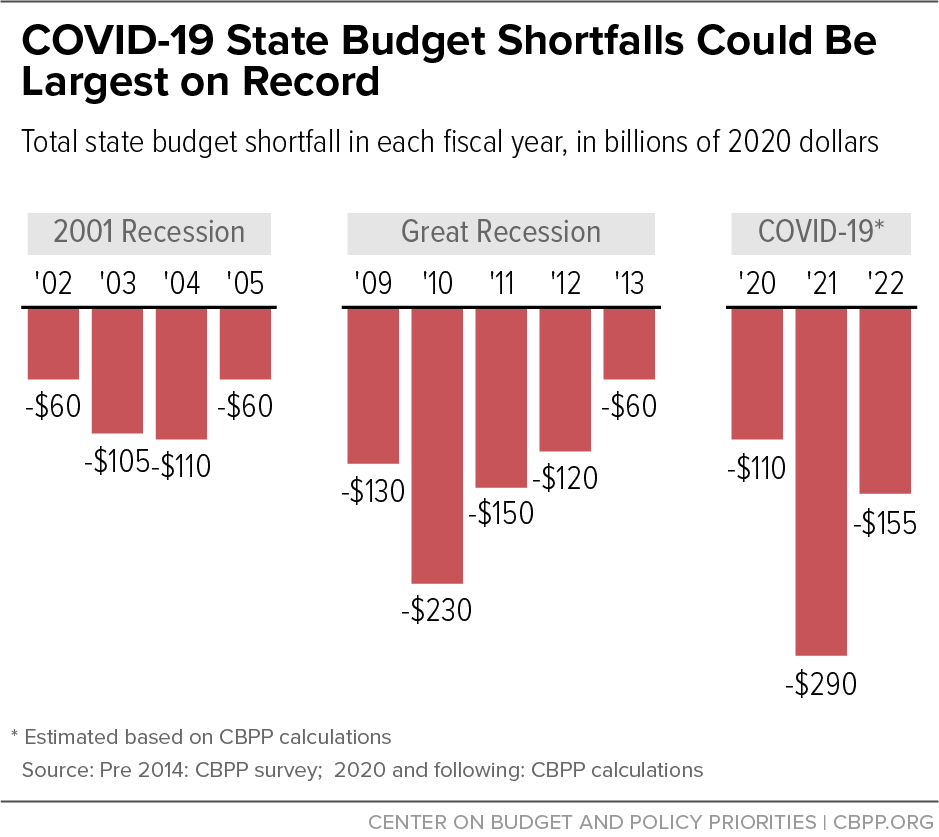

Shortfalls faced by Government Entities

States Continue to Face Large Shortfalls Due to COVID-19 Effects, updated on July 7, 2020.

Our new shortfall figure — which is based on the Federal Reserve Board’s most recent summary of economic projections,2 issued June 10, and the Congressional Budget Office’s (CBO) July projections3 — is lower than our estimate of last month prepared before the updated CBO forecast was released, but higher than our April projection.4

The projected shortfall for 2021 fiscal year, which began on July 1 for most states, is much deeper than the shortfalls faced in any year of the Great Recession (see Figure 1). These figures underscore the continued urgency of the President and Congress enacting substantially more fiscal relief and maintaining it for as long as economic conditions warrant.

…..

Our estimate of $555 billion in shortfalls over state fiscal years 2020-2022 is based on the historical relationship between unemployment and state revenues5 and on the average of the CBO and Federal Reserve Board projections.

So, they are putting these numbers in terms of shortfalls.

I would like to see the total amounts of revenues, year-over-year. They are talking about budget shortfalls, but budgets are fictions, to a certain extent. I would like to see what percentage of the budget these shortfalls represent. Anything to provide a truly meaningful comparison.

The reason I mention this is that certain elements of state expenditures have been creeping up as a percentage of state domestic product (cough, pensions), and other items are likely growing, too. I would like a fair comparison.

State Bankruptcy Revisited

David Skeel has written/advocated for state bankruptcy before. Here’s his recent piece in National Affairs: State Bankruptcy Revisited

During the first debate over state bankruptcy that occurred in the aftermath of the Great Recession, I was a vocal advocate of the idea. As I revisit the issue a decade later, after nearly four years as a member of Puerto Rico’s oversight board, I recognize that the case for state bankruptcy is a bit more complicated than I once imagined. But it remains an entirely compelling one.

….

THE BENEFITS OF A STATE-BANKRUPTCY OPTIONThe irony of the objections that sank the state-bankruptcy option a decade ago — objections that continue to spur opposition to the idea now — is that they are not only mistaken, but each proves to be an argument in favor of the option rather than against it.

The concern that state bankruptcy is simply a ploy to undermine public employees by severely cutting pensions and terminating collective-bargaining agreements is in some respects understandable.

…..

States today do not stand idly by as they tumble toward total collapse. Instead, they take steps to cut costs. Some states raise taxes, and many try to restructure their obligations to existing constituencies. The two constituencies typically hit hardest by these efforts include public employees and the recipients of state services — especially poor and lower-middle-class recipients.

Illinois hasn’t cut nearly enough. Or, really, anything yet.

Rather than permitting states to force the burden onto one or two disfavored constituencies, bankruptcy requires that the sacrifice be borne by everyone. Creditors given collateral to secure repayment of their claims are entitled to priority, of course, but the claims of every class of general creditors — including public employees and most bondholders — can be adjusted. Many years ago, now-Senator Elizabeth Warren pointed to this feature of corporate bankruptcy: “Bankruptcy,” she argued, is “a federal scheme designed to distribute the costs among those at risk.” The promise of equitable treatment — that every constituency shares in the sacrifice — may not be perfectly achieved, but the distribution of the burden is far fairer in bankruptcy than it is outside of bankruptcy.

It depends on the procedure. Because this is a beautiful theory, but hasn’t been borne out by actual municipal bankruptcy experience. So far, only one municipal bankruptcy has ended in the cut of benefits to current retirees.

The outcomes of actual public-entity bankruptcy cases also need to be taken into account in our analysis. During the Detroit bankruptcy in 2013-2014, for instance, were pensions slashed while bondholders rejoiced? Quite the contrary: While severely underfunded pensions were subject to small adjustments — the biggest was the loss of future cost-of-living increases — pensions were otherwise protected. As it turned out, bondholders bore much more of the burden than retirees, with some receiving just 41% of their claims. Other unsecured creditors had their claims cut to 13%. In the Stockton, California, bankruptcy that same year, though retirees were forced to shift to less-generous health-care benefits, pensions were not cut at all. Indeed, the pattern that has emerged across large municipal bankruptcies undermines critics’ claim that bankruptcy would be devastating for pension beneficiaries.

To the extent public employee unions and groups (it doesn’t require to be in an official union to vote one’s own interests) maintain their political power, they don’t need to worry about getting cut more than bondholders.

That reality may step in and they get cut a little, too, well. Politics is the art of the possible, not the art of magic money trees. Unless you’re the federal government.

You can, and should, read the whole thing if you’re interested in the potential for state bankruptcy, but I am still less than convinced.

If the politics allowed for cutting public pensions, then state constitutions would have already been changed (specifically looking at Illinois). State bankruptcy procedures existing will not cause the political will to cut pensions or anything else.

The best way to see this is to look at the morass that is Puerto Rico. Even Skeel recognizes the problem:

The Puerto Rico experience offers one encouraging lesson for those pushing for a state-bankruptcy option, and one that is less encouraging.

…..

The more sobering feature of the Puerto Rico restructuring is its messiness. The oversight board filed the restructuring petition more than three years ago — on May 3, 2017 — and it still is not clear when Puerto Rico will be ready to emerge. To be sure, a relentless stream of natural and manmade disasters — Hurricane Maria, the forced resignation of Governor Ricardo Rosselló, earthquakes, and now the coronavirus — have impeded progress. But the restructuring has been enormously complex on its own.

Also, there is no local political will for cleaning up anything. Last week, there was this story: Puerto Rico announces referendum to protect public pensions. Puerto Rico pensions are essentially pay-as-they-go, and I’m really wondering where all that money is coming from.

There is a reason that Puerto Rico is a fiscal mess, and it’s not the hurricanes. Hurricanes do not make for years of no reliable financial reports. Similarly, there is a reason Illinois is a financial mess and Indiana is not. Choices were made in both places. Simply putting a bankruptcy option in place will not fix Illinois’s dysfunction.

News and opinion compilation

There has been a lot of stuff out there. There will be more.

- Reason: What State and Local Governments Can Learn From the Coronavirus Crisis

- NY: NY Local Sales Tax Collections Drop for Second Quarter of 2020 – Down 27% compared to 2019Q2.

- NY Comptroller: DiNapoli: Trouble Ahead for Local Governments and Schools

- WSJ Op-ed: Blue States Deserve Money From Washington

- Letters responding to that op-ed: Readers Skeptical of Any Blue State Bailout – I agree with ALL the letter-writers.

- NY Comptroller responds to “No Donor” op-ed: New York Really Does Deserve Federal Help – NY has been harder-hit by COVID, and it’s not all di Blasio & Cuomo’s fault. (Though they did make it worse). Anyway, he trots out the bullshit “donor state” stats again. Mr. Comptroller: the federal payroll taxes don’t belong to NY state.

- NYT Op-ed: Congress Struggles With Covid Relief. How That Will Affect Some States and Their Muni Bonds. – The 6 states are: New Jersey, New York, Illinois, Kansas, Oklahoma, Louisiana. The first four, I absolutely agree with.

- Andrew Biggs and Sheila A. Weinberg: A Potential Deal For State Pension Reform – One of those “strings attached” bailout ideas… extending ERISA to public plans, essentially.

- John Bury reacting to the above: Potential Deal for State Pension Reform – I agree with Bury, for all three main reasons.

- Vox: Republicans prepare to unveil long-awaited $1 trillion coronavirus relief package

- Reason: ‘CARES’ Package Part Two Is Coming, to the Tune of at Least $1 Trillion

- Inside Sources: Aid to States Should Include Safeguards and Transparency, Just Like Relief to Businesses

- Bloomberg Law: INSIGHT: Bankruptcy for States? Yes, But Don’t Forget the Constitution

- WSJ: New York Municipalities Feel Budget Crunch as Coronavirus Pandemic Squeezes Funding

- Governing: Here Comes the Hard Part: States, Cities Face Grim Budget Picture

I expect this to bleed well into 2021, no matter who wins election this fall.

Beware of Historical Lessons

And, finally, something from 2015 via Truth in Accounting: The Slow-Motion Financial Suicide of the Roman Empire showing the very old age of the bailout state.

I want to tack onto that piece, though: that “bailout state” of Rome actually continued well beyond the Western Roman Empire… in the guise of the Byzantine Empire, whose inhabitants called themselves Romans and their empire the Roman Empire after the West fell. They had ups and downs of good and some very bad finance, until they, too, finally fell apart…. a thousand years after the Western side did.

It is amazing how long bad public finance can limp along.

And when the bad finance comes to a head, it can end with a bang and not a whimper.

Related Posts

Taxing Tuesday: Bernie Tax!

Taxing Tuesday: Poor Little Rich People and the SALT Cap

Happy New Tax Year!