Around the World in Pensions: Brazil, the EU, and more

by meep

I keep tabs on pension and public finance trends in several threads at the Actuarial Outpost, with my longest-running series being public pensions.

Today, I thought I’d do something different and highlight pension issues outside of the U.S.

BRAZIL: WHEN WILL THERE BE REFORM?

Brazil has had a long-running issue with respect to reforming its pensions. The first piece I noted was this, from May 2016:

Brazil’s Acting President Michel Temer Vows to Tackle Insolvent Pension System

The new government is already talking of raising the retirement age, drawing the wrath of powerful unions and pensioners groups. Senator Paulo Paim, from Ms. Rousseff’s Workers’ Party, or PT, has likened any such move to a war on workers.

“In Brazil, whenever there is a crisis, the first action is to take it out on the working class,” Mr. Paim said. He is leading a group of lawmakers vowing to oppose Mr. Temer’s likely proposal.

What almost no one disputes is that Brazil’s public pension system is in frightful shape. This year it is projected to fall short by 130.8 billion reais (about $37 billion), a 47% increase from its 2015 deficit. The shortfall is projected to soar another 66% to 217.7 billion reais by next year. Brazil already spends roughly 41% of its federal budget on pensions, compared with about 24% in the U.S.

“Brazil is trying to correct a very weakened fiscal story,” said Lisa M. Schineller, an analyst with Standard & Poor’s, one of three major ratings firms that have reduced Brazil’s credit rating to junk since last year. “Clearly, social security is a component that’s weighing on fiscal performance.”

The problem boils down to math: Brazilians retire too soon and contribute too little to generate the benefits they receive.

The average pension is a modest 1,300 reais or $374 a month. But in Brazil, women can retire at age 55 or after working for 30 years, whichever comes first; men can do so at 60 years of age or after 35 years of labor.

The upshot is that the average Brazilian retires at age 54 in a country where life expectancy is 75.7 years and rising. The government calculates that by 2060 there will be only two workers for every retiree, down from a nine-to-one ratio today. Meanwhile, benefits are indexed generously for inflation and GDP growth.

Since then… well, here’s the list of some of the stories I noted, in chronological order. (As some of the original links no longer work, I will link my Actuarial Outpost posts for the non-recent stories)

- Sept 2016: Brazil’s Temer Says Pension Reform Will Not Be Approved Quickly

- Oct 2016: Brazil’s Supreme Court Bars Pension Payouts Rise

- Nov 2016:Brazilian workers outraged over proposed pension reforms

- Jan 2017:Brazil Government Rules Out Changes to Pension Reform Plan

- Feb 2017:Why Pensions Top To-Do List of Brazil’s President: QuickTake Q&A

- Feb 2017:Fixing Brazil’s pension problem

- Mar 2017:Nationwide Protests in Brazil Against Pension Reform

- Apr 2017:Anger Stirs in Brazil as Temer’s Pension Drive Ignores Voters

- Apr 2017:Brazil’s pension reform a crucial signal for investors

- Apr 2017:Brazil Takes Knife to Pension Plan to Ensure Its Survival

- Apr 2017:Brazil waters down pension reform as protests turn violent

- May 2017:Brazil’s Temer acknowledges pension reform still short on votes

- Aug 2017:Brazil’s president expects weaker pension bill to pass: paper

- Aug 2017:Brazil should avoid changes to pension reform bill -minister

- Aug 2017:Brazil chief of staff expects pension reform to pass house in October

- Sep 2017:More Corruption Allegations Mean Brazil Pension Reform Dies Another Day

- Sep 2017:Pension reform in Brazil unlikely before 2019: Itaú economist

- Sep 2017:UPDATE 2-Brazil plans pension vote in October, before tax reform

- Oct 2017:BRAZIL: Delay In Pension Reform May Halt Rate Cuts By The Central Bank

- Nov 2017:Brazil government plans to dilute unpopular pension reform bill

- Nov 2017:UPDATE 1-Brazil central banker urges pension overhaul to avoid market turmoil

- Nov 2017:BRAZIL: Minister Resigns And Boosts Stocks As Pension Reform Hopes Rise

- Nov 2017:Temer Agrees on Brazil Pension Vote With House Chief (agrees on Dec 5-7 dates)

- Nov 2017:Brazil house speaker says whipping votes for pension reform difficult, but urgent

- Nov 2017:Softer Pension Proposal Leads to Brazilian Stock Slip

- Nov 2017:Brazil’s Pension Reform Vote Moves to Dec. 15

- Dec 2017:Lawmaker: Support for Brazil’s Pension Reform More Organized

- Dec 2017: Brazil president sees lower house pension reform vote Dec 18 week

- Dec 2017:Brazilian President: Pension Vote Could Be Delayed to Early 2018

- Dec 2017:Brazil pension vote put off until February

- Dec 2017 :February vote on Brazil pension reform is last chance, house speaker says

- Jan 2018:Brazil President Temer says pension changes remain on agenda

Suuuuure it is. That said, they’ve had a credit rating hit because of all these delays. Brazil is in the junk range for credit ratings — BB- rated by S&P.

BRAZILIAN PENSIONS: THE DIRE NEED FOR REFORM

Going to analysis — this is from April 2017: Brazil’s Pension Reform Proposal is Necessary and Socially Balanced – a piece by the Executive Director of the World Bank, has key charts.

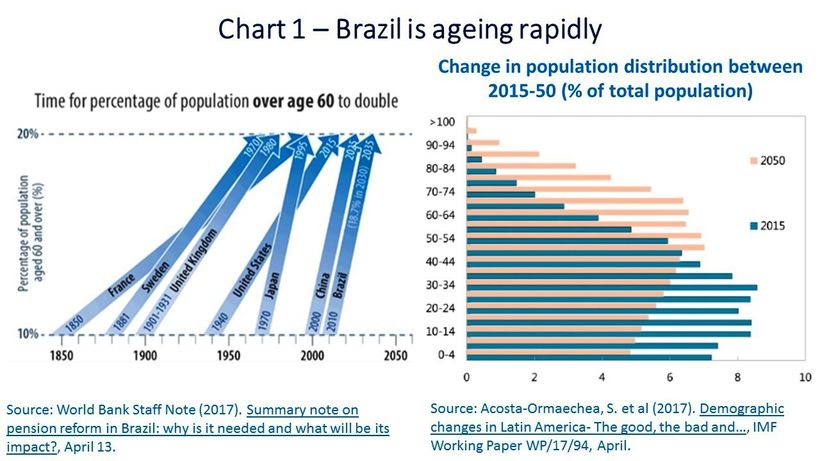

Brazil is ageing rapidly. Its share of the population over age 60 is doubling in a short time span as compared to previous country experiences (Chart 1 – left side). Increases in life expectancy and falling fertility rates explain such a development. The age distribution of the population is bound to feature rising proportions of older people over time (Chart 1 – right side).

…..

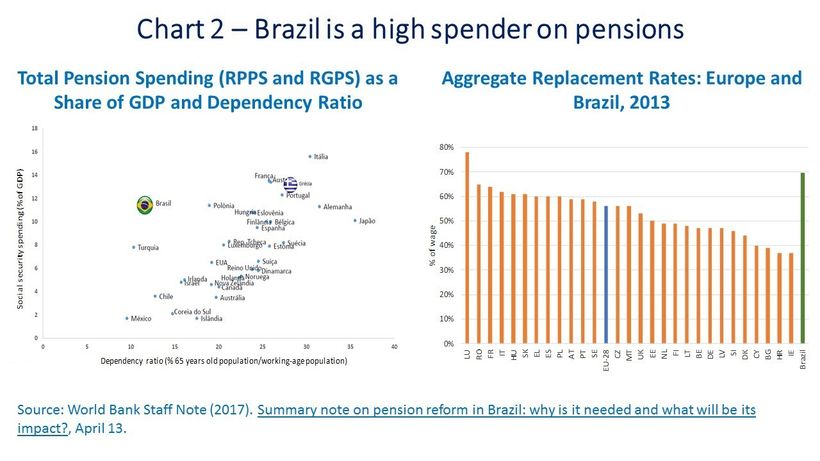

Brazil is a high spender on public pensionsBrazil’s demographic evolution is taking place over a public system where payments of benefits have been proportionately high as compared to other countries. A complimentary pillar of voluntary pension savings accounts has been gradually created. On the other hand, added benefits paid by the two separate pension regimes – for private sector workers (RGPS) and public servants (RPPS) – as a proportion of GDP stand out as relatively high when matched with the still relatively low age-dependency ratio (Chart 2 – left side).

…..

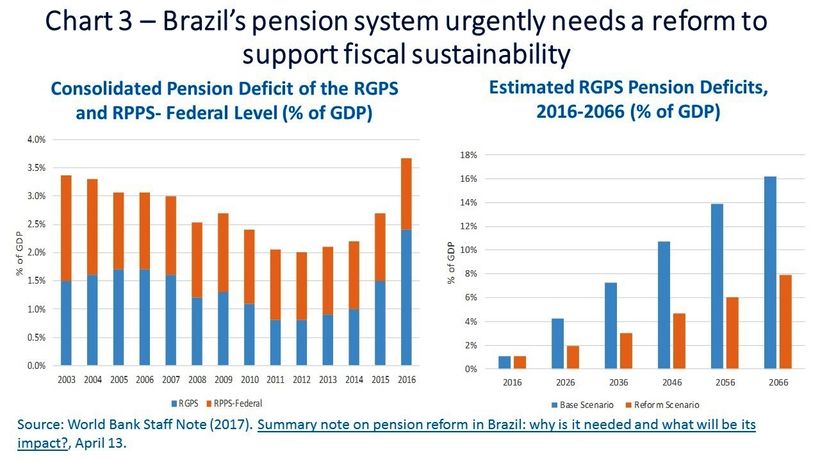

Brazil’s pension system urgently needs a reform to support fiscal sustainabilityThe Brazilian public defined-benefit pay-as-you-go pension system has already exhibited deficits for some time (Chart 3 – left side). The upward trajectory of latter years reflects to some extent the negative impact of the likely non-recurrent extraordinarily deep dive of employment, wages and corresponding pension contributions of the period. On the other hand, the deficit dampening during the “boom of the new millennium” also reflected a non-recurrent increase of labor formalization and a step-change of unemployment levels from 11% to 5% of the labor force (Canuto, 2016). Demographic dynamics will play out upon a basis where pension benefits are already larger than actual contributions.

So here we are, about a couple years later, and the reform is still not done.

And it still needs to be done.

One item that kept popping up in stories was that this system has no minimum retirement age. I didn’t dig into the details of the benefits, but I assume there are various adjustments for early retirement… just as we have with Social Security.

Even so, you can’t get your own Old-Age Social Security benefit before age 62. I can see what the average retirement age had been 54 in Brazil. Even if their life expectancy is about a decade shorter than the U.S., that doesn’t mean such early retirement ages are supportable.

PENSIONS ARE A WIDE LATIN AMERICAN PROBLEM

Here is a Bloomberg View piece called “The Pensions That Ate Latin America — it’s not only Brazil that has a problem, but also Chile and Argentina. (we are all ignoring Venezuela, which has much worse problems)

A few items from that piece.

Long hailed for its youth and vigor, Latin America is graying fast, raising the specter of fiscal crisis as retirees outnumber the able-bodied workers required to support them. Yet even as a new generation of national leaders seeks to shore up a shaky pillar of the social contract, a rebellion against pension reform is in full cry.

Chileans poured into the streets ahead of this year’s election to roll back free-market-inspired reforms conceived under former dictator Augusto Pinochet. Thousands of Argentines banged pots and pans against President Mauricio Macri’s overhaul of the loss-making pension system that passed congress last month. It’s no better in Brasilia, where a political insurrection is in bloom over pension fixes designed to rescue the country’s fraught finances, and maybe the mandate of beleaguered President Michel Temer in the bargain.

….

The population aged 60 and over in Central and South America and the Caribbean is set to overtake those aged 15 and under by 2036. By mid-century, the elderly will account for 26 percent of Latin America’s population, about the same share of grayheads as in the most developed countries today. The fastest growing segment of the population? Those over 80.….

What’s worse, the region’s pension systems are as perverse as they are profligate, hoovering up money to disproportionately benefit the most privileged groups. Once again, Brazil sticks out: The richest 20 percent of retirees pull in 53 percent of total pensions — or 10 times the amount pocketed by the bottom fifth — according to the finance ministry. No wonder Catholic University economist Jose Marcio Camargo branded Brazil’s trickle-up social security system one of the largest income transfer schemes from poor to rich on record.

…..

Public-sector employees are a caste apart. Honors to Brazil’s 980,000 federal pensioners: They not only punched out early, but cost taxpayers as much as 32 million private-sector retirees — and yet they fiercely oppose even the government’s modest proposal to set a minimum retirement age. “In Brazil, only the poor work until age 65,” University of Sao Paulo economist Paulo Tafner told me.…..

In fact, because 130 million Latin American jobs — and half of all non-farming employment — still fall under the legal radar, contributions to social security are irregular, by employees and employers alike. Levy reckons that up to one in five workers move back and forth between formal and informal jobs every year.

That’s pleasant.

U.S. Social Security definitely has a problem, but it’s not as bad as Brazil’s similar program.

EUROPEAN UNION PENSIONS NEED A BAILOUT

I find this completely expected.

EU pension fund on brink of collapse: Taxpayers will have to bail out hundreds of MEPs

Before I dig into this, legislators should not be given pensions. Nor should governors. Nor any elected official. I have seen arguments for (if they’re deciding contributions to public pensions, you want them to have skin in the game), but I have had it. Being an elected official should not be a career. It should be a sometime thing. You do it for a short stint, you save up for your own retirement privately while doing it, and then you go back to some productive job.

People should not be encouraged to sit around in these seats. If we can’t get term limits, we should at least reduce their privileges.

Okay, now the piece:

Germany’s biggest newspaper Bild reported it has seen paperwork indicating a shortfall of millions of euros which means the pension fund will collapse by 2026 at the latest.

It cited an internal opinion of the Secretary-General of the European Parliament, Klaus Welle, for the Committee on Budgetary Regulation.

The endangered fund closed to new members in 2009 and, by the end of 2016, held assets worth €146.4 million.

But by then the fund’s liabilities – the outstanding pension entitlements of the lawmakers – already stood at a staggering €472.6 million.

Wow, that’s Kentucky levels of fundedness.

Even back in early 2009 the lavish and controversial supplementary pensions of MEPs were in deficit to the tune of €120 million. Now it is nearly three times that amount.

“The estimated date of insolvency of the voluntary pension fund is roughly estimated between 2024 and 2026”, according to the documents seen by Bild.

If the fund’s assets only generate a 2 per cent return per year it will not be solvent beyond 2024.

According to Bild, more than 700 MEPs lay claim to a pension from the fund. By the end of 2022 alone, 145 of them will retire.

If the fund goes bankrupt, the European Parliament will be legally responsible for the deficit, meaning the costs will be left for the taxpayers of the EU to pick up.

These supposedly are legislators, representing various countries at the EU Parliament.

I’ve got an idea: push these obligations back onto the countries where these MEPs came from. Seems only fair.

SPAIN: ALSO IN PAIN

Via Allison’s Ode to the Second Moment (a little newsletter I recommend subscribing to), I see Spain also has issues:

You may not have heard about it, but Spanish pensions are in deep trouble—serious trouble. Spanish state pensions have a terrible combination of being exceedingly generous, an average 83% replacement rate, and facing unfavorable demographics, Spain has the world’s second oldest population after Japan. Reforms in 2013 increased the retirement age and encouraged people to work longer. But a generation of young, marginally-employed Spaniards means less tax revenue and a reckoning may be coming even sooner than projected.

The Socialist government proposed a financial transaction tax to help pay for pensions. This seems counter-productive to me. It is not realistic to rely on the government and younger taxpayers to finance generous pensions for all. Spain needs to diversify its sources of retirement income. About 50% of Spaniards receive some form of pension benefit from their employer, either a Defined Benefit or a Defined Contribution, but the contributions to these plans are small. Of course they are! Why would anyone bother contributing to a pension account at work if they expect a pension with an 83% replacement rate from the government?

Excellent question.

The replacement rate from Social Security, by the way, is lower than Spain’s, but it’s actually pretty good if you happen to be low income.

Checking out the most recent calculations, and just looking at those taking benefits at age 62, those with very low earnings can get a replacement rate of about 60%, medium earnings gets you about 30%, and maximum earnings (somebody like me, who goes over the cap), gets about 20%. You can look at the tables to get the exact amounts.

It’s not shabby, but not fabulous. There’s definitely an upside to saving for retirement, even if Social Security sticks around as-is.

Here is the OECD study Allison links to, (and awesomely, if you click the links to the figures, you get a spreadsheet with everything in it), so let me pull a few specific graphs.

Here is the Old Age Dependency Ratio:

Note who also has a very high dependency ratio projected for 2015: Japan, Italy, and South Korea. This is a ratio of the number of people over age 65, compared to those age 20-64. It does not actually show how many non-working old people versus workers. I don’t know about other countries, but many people over age 65 work for pay in the U.S.

Now, the current old age dependency ratio for Spain is only a little higher than the United States. I find that interesting. The Spanish are getting older faster than the U.S., because there are more kids being born in the U.S. and probably due to projections related to immigration.

According to the CIA World Factbook, the total fertility rate for Spain is 1.5 children per woman; the TFR for the U.S. is 1.87. Japan is 1.41.

Here is the reitrement income replacement rate:

I will note that the Netherlands is pretty much at 100% replacement. Italy and Portugal are also fairly high.

NETHERLANDS PENSIONS: ARE THEY AS GOOD AS THEY SAY?

Recently, one person noted a Dutch pension fund crowing about its great results:

The headline from the Dutch business newspaper Het Financieele Dagblad caught my eye on Twitter a few weeks ago: “America is the example of how not to do pensions.” 1 The quote was from an interview with Angelien Kemna, who stepped down on Nov. 1 from the top finance job at APG Groep NV, which manages the Netherlands’ biggest (and world’s fifth-biggest) pension fund. After reading it, it struck me that it might be useful to let U.S. readers know what one of the leading figures on the global pension scene thought was wrong with the way this country handles retirement savings. 2

The Dutch retirement savings system, considered one of the world’s best, is built around defined-benefit workplace pensions — as the U.S. system used to be. But while some pension funds are affiliated with a single company, such as Royal Dutch Shell PLC or Koninklijke Philips NV, industry-wide pension arrangements are the norm. APG manages ABP, the 405 billion-euro pension fund for workers in the public sector and education, and several smaller funds.

….

Justin Fox: Why is America the example of how not to do pensions?Angelien Kemna: What I saw living in the United States was that so many people not only lost their jobs and houses during the financial crisis, they also lost more than half of their pensions, because their pensions were 401(k)s. These are individualized pensions with high fees. People don’t understand the risks they take, they do not share risks over generations. It makes them extremely vulnerable in an area that is very important for them — their future life and safeguarding their future life.

…..

JF: One thing that seems under-understood here is that it’s not just the competence issue of whether individuals are good at investing for retirement, it’s that in theory — and I think in practice in the Netherlands — it’s cheaper to do it collectively, right?AK: Oh, absolutely. And yes, we also suffered from the crisis as pension funds, but de minimis. We’ve totally recovered from the crisis, and I would say that the system has been shown to be pretty robust under market crises. Our system is less robust under longevity risk.

….

JF: In the U.S., the place where there are still defined-benefit pensions is mostly with state governments, and there’s lots of pressure politically for the states to go individual, in part because they’ve done a pretty poor job in general of setting aside enough money. It seems like the Dutch and a few other Northern European countries have this unique mix of a sense of “We’re in this together,” but at the same time a really hard-nosed accounting tradition. That’s hard to replicate.AK: Yes, the majority of the state defined-benefit systems in the U.S., if they would have to apply our regulatory rules, they would be seriously underfunded. It’s very hard to invest your way out of that, so they do need to do something.

…..

JF: In both these systems, unexpected things happen — you have a market crash or life expectancies keep growing. The advantage of a 401(k) system is that it’s supposedly not the government’s problem, although they might end up with a lot of very poor 80-year-olds 20 years down the road. With the defined-benefit system, if you can make adjustments like that, that’s the better way to go. I think the problem with state pensions in the U.S. is that both politics and, in Illinois, the state constitution are preventing them from making even the slightest adjustments.AK: It takes us forever, but over the years, continuously, adjustments have been made so that our pension system would stay affordable. We went from a pension based on your last earned income to pensions based on average income over your lifetime. That’s a huge difference, but it went pretty smoothly. Now we’re not giving extra pension if your income is above 100,000 euros, and that also went pretty smoothly. So it’s not easy, but being able to have some flexibility is necessary.

Now, there are definitely good points about the Dutch retirement system. They do have some good risk sharing levers, and having lifelong retirement income is very important. The adjustments they’ve made to the benefit calculation makes it stable.

But I want to note that I’ve seen the Netherlands pension funds have been getting in on the divestment action, and it goes beyond the usual “Oil is evil” — for example, the largest Dutch pension funds divested from some Israeli banks in 2014, due to them financing the building of Jewish settlements. It’s bad enough they’re doing the carbon reduction thing, too.

So while individuals might make those kinds of decisions for themselves, because they don’t like particular industries, what happens with these large piles of pension money is they become attractive to political actors who are not the ones going to be hurt when divestment hurts the pensions’ returns.

So we will see if the Dutch pension system maintain its position as the best retirement system in the world.