Treasury to Central States: You Didn't Cut Enough

by meep

Perfect news drop for a Friday afternoon in spring, when people have more fun things to pay attention to. Especially the day after Cinco de Mayo.

The Treasury Department on Friday denied the benefit reduction application of the $17.8 billion Teamsters Central States, Southeast & Southwest Areas Pension Fund, Rosemont, Ill.

In a letter to the pension fund board of trustees, Treasury Special Master Kenneth Feinberg said the application was denied for failing to meet three criteria of the Kline-Miller Multiemployer Pension Reform Act of 2014, which created the benefit suspension process.

Central States’ proposed benefit suspensions “are not reasonably estimated to allow the plan to avoid insolvency,” Mr. Feinberg said, because Treasury officials considered the plan’s 7.5% rate of investment return and entry age assumptions to be unreasonable. “We found there were fatal flaws in this submission,” he said on a press call.

The plan also did not distribute benefit cuts equitably, and did not provide participants with easily understood notices, according to the letter.

The pension fund applied Sept. 25 for permission to reduce benefits in order to avoid insolvency that it projected would happen by 2026. At the time of its application, it was 53% funded, with $35 billion in liabilities.

A copy of the letter can be found here.

EXCERPTS FROM THE LETTER

John Bury has pulled out his preferred excerpts, including that the valuation approach is a bit optimistic (including a 7.5% return assumption, which is lower than most public pension assumed returns); that the cuts proposed aren’t equitable; and that the notices are too confusing to normal people.

Here’s one of the excerpts Bury pulls:

Application of Special Limitation on Suspension of Benefits Specifically, Treasury has concluded that it is not reasonable to justify larger benefit suspensions for one group of UPS participants based on the fact that those participants are not covered by a make-whole agreement (and therefore are less protected from benefit cuts) than for another group of UPS participants who are covered by a make-whole agreement (and thus are more protected from benefit cuts). Applying a factor in a manner that justifies larger cuts for participants who are otherwise less protected (and therefore stand to receive smaller benefits) is not a reasonable application of the factor.

So… you shouldn’t cut the people who are less protected? scratches head Okay, I guess.

I’ve not seen the notices Central States sent out, so I cannot comment on that.

I will pull my own favored excerpts that differ from Bury’s:

Under the Act, Treasury, in consultation with the Pension Benefit Guaranty Corporation (PBGC)

and the Secretary of Labor (DOL), must approve an application upon finding that the plan is

eligible for the benefit suspensions and has satisfied the applicable statutory requirements. 1 The

Act requires, among other things, that the proposed benefit suspensions be reasonably estimated

to allow the plan to avoid insolvency? Put another way, a key test for any application under

Kline-Miller is whether the proposed benefit suspensions take a plan off the path to insolvency.

As described further below, Treasury finds that the Plan’s proposed benefit suspensions are not

reasonably estimated to allow the Plan to avoid insolvency.…..

I. Suspension Must Be Reasonably Estimated to Avoid InsolvencyKline-Miller provides that:

“[a]ny suspensions of benefits under a plan, in the aggregate . . . , shall be

reasonably estimated to achieve, but not materially exceed, the level that is

necessary to avoid insolvency.”To demonstrate that a suspension satisfies this requirement under the regulations implementing

this provision, an applicant must use actuarial projections. One type of required projection is a

deterministic projection of cash flows, under which the plan’s asset balance is projected forward

using assumptions regarding the amounts of money coming into the plan (e.g., contributions,

withdrawal liability payments, and investment returns) and going out of the plan (e.g., benefit

payments and administrative expenses). A second type of projection, required for the largest

plans, is a stochastic projection, which also projects the plan’s asset balance going forward using

assumptions. However, the stochastic projection does not use fixed assumptions for the rate of

investment rehtrn, but instead projects a range of possible outcomes to take into account the

variability of investment returns.Treasury evaluated the assumptions and methods used in the Application based on the

regulations. The regulations require that each of the achtarial assumptions or methods, as well as

the combination of achtarial assumptions and methods, used for the required actuarial projections

be reasonable, taking into account the experience of the plan and reasonable expectations.5 In

applying the regulations, Treasury referred to guidance provided by the standards of the actuarial

profession (primarily Actuarial Standards of Practice (ASOPs) numbers 4, 27 and 35).The regulations and ASOPs require that, to be reasonable, each of the assumptions or methods

must be appropriate for the purposes of these cash flow projections (which means, among other

things, that factors specific to these cash flow projections must be taken into account). The

ASOPs also require taking into account historical and current economic data that is relevant as of

the measurement date and require that assumptions have no significant bias. The actuary also

must consider the materiality of the assumptions and the balance between the benefits of using

refined assumptions (that is, assumptions that are based upon more extensive and specific study

and research) and the cost of using those refinements.Treasury has concluded that two of the assumptions used for the actuarial projections in the

Application are not reasonable.

And then explains that the investment return assumptions (7.5%) and then Entry Age assumption is also unreasonable. I will not comment on the second, but wowee on the first one.

REASONABLE RETURN ASSUMPTIONS?

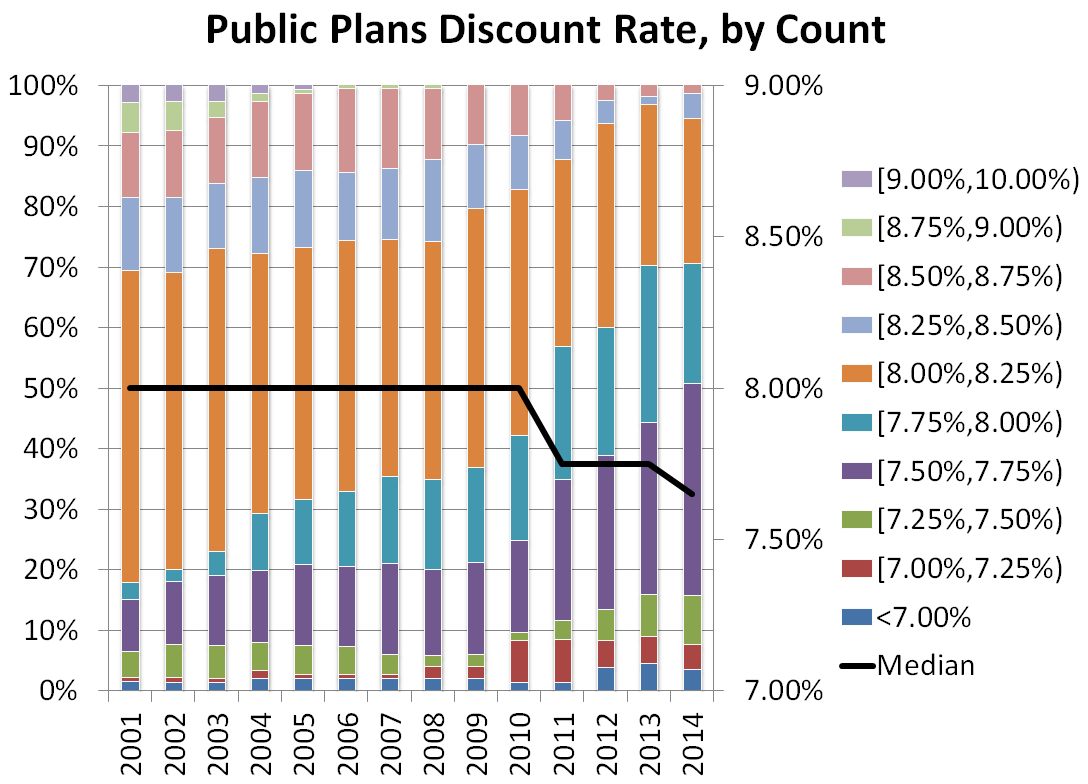

To remind, this is what the discount rate (which is the same as the return assumption in these approaches) used by public plans in the public plan database look like – to make it simple, I’ll use the graph by count:

For the longest time, the most popular discount rate was 8%. Just recently, the median dropped to 7.75%.

Fewer than 20% of the public plans use a discount rate less than 7.5%.

And here we have:

Relevant Current Economic Data Not Taken into Account

The investment return assumptions used in the Application do not adequately take into account

relevant current economic data. Relevant current economic data (i.e., including near-term

current investment forecast data for each asset class) must be reviewed to determine whether

refined investment return assumptions would be expected to produce materially different results.A review of relevant current economic data clearly demonstrates that refined investment return

assumptions that take into account appropriate investment forecast data regarding expected near term

rates of return would be expected to produce materially different results. For example,

commenters, as well as the Plan, used the Horizon Survey of investment forecasts of 29

investment professionals for purposes of comparison. In comparison to the Horizon Survey data,

the Plan’s investment return assumptions are in excess of the 1 0-year 50th and 75th percentile

survey results for every asset class. For the Plan’s total portfolio, the estimated 10-year average

rate of return based on 10-year average expected results for the corresponding asset classes in the

Horizon Survey is estimated to be 6.43% — a full 123 basis points less than the 7.66% average

annual rate of return for the portfolio based on average expected rates of return for the Plan’s

asset classes provided by the Plan.…..

Bias

The investment return assumptions used in the Application do not satisfy the requirement that

assumptions have no bias (i.e., not be significantly optimistic or pessimistic) outside of narrowly

specified circumstances. The assumptions are significantly optimistic, as evidenced by the

available relevant investment return forecast data in the Horizon Survey described above, which

the Plan cites as supportive of the reasonableness of its investment return assumptions.

Well, well, well.

SOLUTION: CUT MORE

But here’s the thing: the special master here is saying that they were too optimistic in their approach. The other items – in terms of equity of spreading the cuts and communications – are simpler fixes.

But having to cut more after all this controversy?

Ooooof.

Look, the plan goes bankrupt (as in no money) in 10 years with optimistic assumptions before the cuts. They’re in an asset death spiral. This is not going to fix itself.

If they just let the money run out and then try to put the plan on PBGC, the retirees will get extremely little.

When those funds run out of money to pay benefits, it will be up to the P.B.G.C. to step in. It now pays a maximum of $12,870 a year for workers who spent 30 years digging coal or driving trucks, even if the plan called for larger payouts. A worker with only 15 years of service gets half of that.

So more minor cuts now compared to the devastating cuts in less than ten years… Nyhan needs to get cracking.

And do better with the notices, dude.

Related Posts

Taxing Tuesday: Let's Sue the Feds!

Good News for Monday: Locks Unlocked

Divestment and ESG Follies: Mandating Women on Corporate Boards