Setting the Stage for 2017: Looking at Social Security

by meep

Welcome to 2017! This week, I want to set out some of the themes I want to cover this year, even if it never makes political news.

Let’s start off with that perennial: Social Security, and how it’s going to run out of money. Or not.

CURRENT SOCIAL SECURITY PROJECTIONS AND LAW

The Congressional Budget Office came out with some projections recently.

Future of Social Security Benefits in Question:

SS benefits are on par for a 31% reduction by 2029, CBO reports.

The Social Security Administration is on course to run out of money, says the Congressional Budget Office (CBO.)CBO projected a 31% reduction in scheduled payable benefits by 2029 and a 29% reduction by 2060, given current credited outlay limits.

The CBO prepared long-term projections and concluded if the current revenues were insufficient to cover benefits, the Social Security Administration would no longer be permitted to pay full benefits.

“After increasing for several years, the required reduction would abate as people in the baby-boom generation died,” says the report. “And because life expectancy is anticipated to continue to rise, by 2080, [benefits] would need to be 34 percent lower.”

Most (73%) of the 61 million people who receive Social Security benefits are retired workers or their spouses and children, and another 10% are survivors of deceased workers.

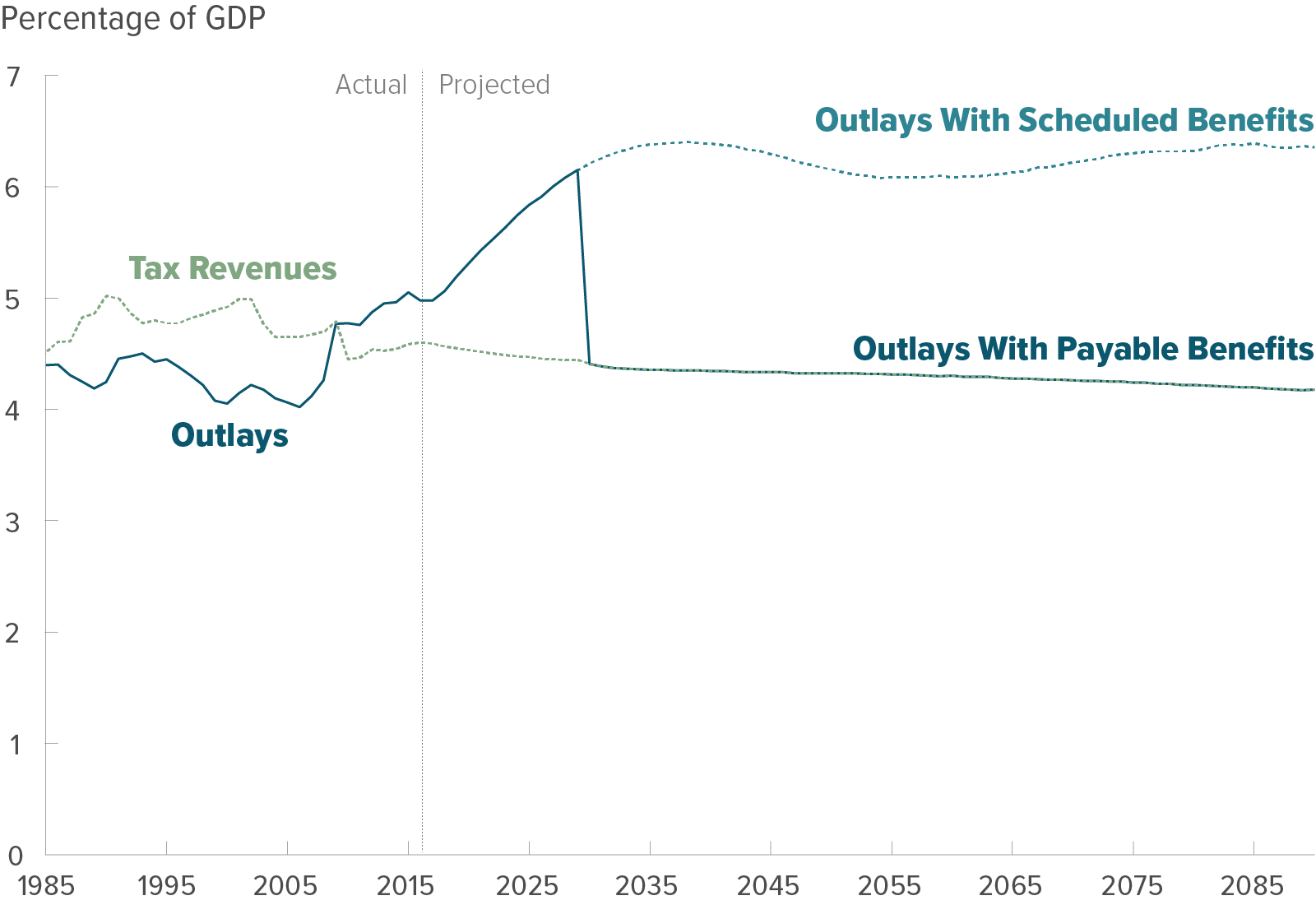

“In fiscal year 2016, total outlays exceeded noninterest income by about 7 percent,” according to the report. “If current laws governing taxes and spending stayed the same and if benefits were paid as scheduled, outlays for the Social Security program would rise from 5.0 percent of gross domestic product (GDP) in 2016 to 5.9 percent in 2026 and to 6.3 percent in 2046; they would exceed tax revenues by 33 percent in 2026 and by 42 percent in 2046.”

The CBO report can be found here, with this being a link to the full PDF.

Let’s check the key graph of projections:

You need to know that current federal law is such that when the Social Security Trust Fund runs out, the benefits are supposed to be automatically cut to match the current payroll taxes coming in.

You may recall that in 2011/2012 the Social Security-related payroll tax was whacked by two percentage points, which would normally have whacked at the Trust Fund. It did not because Congress said we’ll pay for it out of the General Fund.

Basically, those “automatic” cuts ain’t happening. They’re there as a perpetual boogieman, though Congress will just keep messing with the legislation to make sure those cuts don’t happen directly.

Another item from the CBO: Retirement Assets Among Many Potential Targets for Tax Reform

The large annual budget deficits projected under current law have many tax experts contemplating ways the federal government could bring in additional revenue; the Congressional Budget Office (CBO) has published a paper exploring more than 100 potential avenues for reform.

The extensive research paper estimates the budgetary effects of each approach and highlights some of the advantages and disadvantages of each, including options that would impact the tax treatment of assets allocated pre-tax for retirement.

One such option suggested is to “tax Social Security and Railroad Retirement benefits in the same way that distributions from defined benefit pensions are taxed.” According to CBO researchers, “under current law, less than 30% of the benefits paid by the Social Security and Railroad Retirement programs are subject to the federal income tax. Recipients with income below a specified threshold pay no taxes on those benefits. Most recipients fall into that category, which constitutes the first tier of a three-tiered tax structure.”

The researchers further note that if the sum of this group’s adjusted gross income, their nontaxable interest income, and one-half of their Social Security and Tier I Railroad Retirement benefits exceeds $25,000 (for single taxpayers) or $32,000 (for couples who file jointly), up to 50% of the benefits are taxed. Above a higher threshold—$34,000 for single filers and $44,000 for joint filers—as much as 85 percent of the benefits are taxed.

The paper continues: “By contrast, distributions from defined benefit plans are taxable except for the portion that represents the recovery of an employee’s basis—that is, his or her after-tax contributions to the plan. In the year that distributions begin, the recipient determines the percentage of each year’s payment that is considered to be the nontaxable recovery of previous after-tax contributions, based on the cumulative amount of those contributions and projections of his or her life expectancy. Once the recipient has recovered his or her entire basis tax-free, all subsequent pension distributions are fully taxed … Distributions from traditional defined contribution plans and from individual retirement accounts, to the extent that they are funded by after-tax contributions, are also taxed on amounts exceeding the basis.”

CBO suggests this tax reform approach would treat the Social Security and Railroad Retirement programs in the same way that defined benefit pensions are treated—by defining a basis and taxing only those benefits that exceed that amount. For employed individuals, the basis would be the payroll taxes they paid out of after-tax income to support those programs (but not the equal amount that employers paid on their workers’ behalf).

…..

Under this reform option, the FRA would continue to increase from age 67 by two months per birth year, beginning with workers turning 62 in 2023, until it reaches age 70 for workers born in 1978 or later (who turn 62 beginning in 2040). As under current law, workers could still choose to begin receiving reduced benefits at age 62, but the reductions in their initial monthly benefit from the amounts received at the FRA would be larger, reaching 45% when the FRA is 70.CBO researchers speculate that any increase in the FRA “would reduce lifetime benefits for every affected Social Security recipient, regardless of the age at which a person claims benefits. A one-year increase in the FRA is equivalent to a reduction of about 6% to 8% in the monthly benefit, depending on the age at which a recipient chooses to claim benefits. Workers could maintain the same monthly benefit by claiming benefits at a later age, but then they would receive benefits for fewer years.”

We’ll see if these get anywhere. I don’t see making Social Security more taxable for low income seniors is going to go over politically at all.

SOCIAL SECURITY SALARY CAP

This is from 2014, but I saw it bubble up on facebook again recently:

Here’s the deal: for the longest time it has been those on the left who have wanted to make sure that salary cap stays in place.

The cap for taxation for Medicare was removed in 1993, as part of the “reform” during the Clinton years that included making more of Social Security benefits taxable.

But they didn’t remove the salary cap for Social Security. Have you ever wondered why that cap is there?

First off, note that few people are above that cap currently:

Disclosure: I’m one of those few above the cap, and even with the 7% bump of the cap for 2017, I should still be above the cap. Part of that is because I’m an actuary and part of that is because I have 3 revenue sources currently.

But here’s the deal: people with really high incomes/revenue streams generally have a lot of control over how they take that income.

But let’s push that back for a moment.

From a few years back — What Impact Would Eliminating the Payroll Cap Have on Social Security?

Question: How much revenue would come into the Social Security Trust Fund each year and how far out would Social Security solvency be extended if the payroll cap were to be eliminated?

Paul Solman: I’ve just gone back to a story we did on this very subject back in 2005 with Columbia finance professor Stephen Zeldes, “Raising Tax Cap Explored as Way to Close Social Security Gap,” and here’s what I reported at the time:

“Removing the cap entirely, thereby imposing a flat tax of 12.4 percent on all earnings — essentially a $100 billion a year tax increase on the wealthy — would more than completely close the funding gap.”

More recently (Septempter 2010), here’s what Janemarie Mulvey wrote in a report for the Congressional Research Service:

“If all earnings were subject to the payroll tax, but the base was retained for benefit calculations, the Social Security Trust Funds would remain solvent for the next 75 years.”

Now, that’s 7 years ago and the number no longer hold… but it’s pretty close.

PLAY THE SOCIAL SECURITY GAME

The American Academy of Actuaries has put together The Social Security Game with more recent proposals and numbers, so you can see what can close the gap.

Here are the choices you can make:

Benefit cuts:

- Increase full retirement age

- Reduce COLAs

- Reduce benefits for future retirees

- Lower benefits for future high-income retirees

Revenue increases

- Increase payroll tax

- Subject higher wages to payroll taxes

- Subject benefits to higher taxes

- Apply payroll taxes to health insurance premiums

You can go play the game yourself; most of these options have multiple things you can choose, such as the amount to increase taxes or to decrease benefits.

I am picking one choice: removing the salary cap for payroll taxes, but keeping the cap for benefits.

It fills the gap 88%.

I believe that one item makes the biggest difference, but I’ll look at that in a future post.

SOCIAL SECURITY BECOMES OLD-AGE WELFARE

Here’s why many people of any political persuasion resist making Social Security means-tested: because that means Social Security becomes old age welfare… and not something one has “earned”.

As a matter of legality, one hasn’t “earned” anything by paying those OASDI taxes all those years. Congress can change the law as to the SocSec benefits at a whim — and they have changed it loads of times before.

But that’s legality, not politics. And it’s definitely not how people feel about “their” SocSec benefits. They feel they have earned the benefits, as it’s taken as a straight percentage of their wages (as opposed to the bizarre alchemy of federal income tax calculations) and the benefit is directly related to what they “paid into” the system.

Here are arguments from the right on why the cap shouldn’t be raised. That’s from Andrew Biggs, who I generally agree with re: public pensions, etc. More from the Heritage Institute, also on the right.

Some of that is assuming that the cap would be removed for both the benefit and the tax, which doesn’t follow at all.

Here is something from the left (or at least the non-right):

“Why Aren’t Social Security and Medicare Means Tested?”

….. First, the program’s benefit formula favors lower-wage workers. Benefit amounts are based on the lifetime earnings history. The first dollars of a worker’s wages are replaced at a 90 percent rate. Earnings in a second bracket (mechanically like an income-tax-rate bracket) are replaced at a 32 percent rate. And any earnings above that level are replaced at only a 15 percent rate. Thus, although higher-wage workers receive more dollars in absolute terms, they receive less back in Social Security benefits per dollar of tax paid over their lifetimes. At the extremes, the difference in the implicit rate of return on those contributions is enormous.

…..

Thus, people who call for “means testing” of Social Security and Medicare are just a little late; means testing is already there. In fact, it arguably was embodied in the original features of both programs, and it has been made only more pronounced over time.

…..

And finally, although Social Security has always aspired to provide at least a fair return on taxes paid by all income groups of workers (understanding that because of the annuity nature of the program, longevity will play a major role in determining the return for any particular worker), that aspiration is being challenged – notably for high-wage retirees. The ideal of an investment return for all that is at least fair helps to maintain a societal consensus in support of the program. Conversely, the pressure that we sometimes feel from people who perceive that their own interest would be better served if they could opt out of the program threatens to undermine its political viability in the long term.

This has been the main reason that even those on the left have been wary of removing the salary cap for taxes and keeping it on benefits — if you decouple the benefits and the taxes, then it becomes more obviously income redistribution and thus less popular. Most politicians would rather not Social Security become yet another welfare program.

A lot of the means-testing rhetoric has come from the right, not the left. Most of the opposition to means-testing comes from liberal groups.

While some find it easy to say that wealthier individuals should not receive Social Security because they do not need the income in retirement, means-testing the program is much more complicated and could result in a fundamental transformation of Social Security as we know it. It would no longer be an earned right, and the benefit would no longer be related to contributions.

It was never an earned right. Every time I see that verbiage, I assume some bullshit is about to be pulled.

I think there will be more means-testing on Social Security, whether indirect or direct, because that’s what will be sustainable.

I think the most likely will be removing the cap on payroll taxes while maintaining it on benefits – this will affect me negatively, so obviously I don’t like this solution.

However, the “crisis” in Social Security is not seen as an immediate crisis. I’m not expecting a lot of movement on this in 2017, but we’ll see. I will be revisiting Social Security-related themes even if it gets no political play this year.

Related Posts

Federal Tax Avoidance Follies: A Splash of Reality

Taxing Tuesday: What's the Real Tax Rate?

Mornings with Meep: What Exactly is a Fiscal Crisis? When Does It Happen?