Chicago Pensions: Drowning, Not Waving

by meep

Let’s see the latest news about Chicago pensions:

Yvette Shields of Bond Buyer: Investment losses sting Chicago pensions, 2022 balance sheet

Investment losses last year eroded funding ratio gains achieved a year earlier by Chicago’s pension system, casting a shadow over a healthy pickup of taxes on the city’s audited financial results.

The city’s overall net position for accounting purposes deteriorated to negative $27.6 billion in 2022 from negative $27.1 billion in 2021 due to growth in the pension liabilities. It hovered between negative $28.4 billion and negative $29.5 billion between 2017 and 2020.

….

The net pension liability, or NPL, rose to $35.4 billion from $33.7 billion as the funds were stung by double-digit investment losses, and the upward trajectory continues a trend as the NPL figure had risen from $32.96 billion in 2020.

….

“Even with the recent progress on pension funding, however, the city of Chicago still has the lowest funded ratios of any large city in the country,” the April budget forecast read. “The city’s pension funds are at an average 23% funded ratio and an extended economic downturn and poor investment performance in FY2022 could have created near-term solvency issues for the pension funds in their ability to pay pensions.”

Between 2014 and 2023, the city increased its pension contributions by $2.2 billion, $1.3 billion of which occurred in the last four years.

By the way, this does not include the Chicago Public Schools’ pensions. The funds included in the above:

- Police: https://chipabf.org/fund-reports/

- Municipal workers: https://www.meabf.org/financial-reports/

- Laborers’: https://www.labfchicago.org/publications/fund-reports/

- Firefighters: https://www.fabf.org/FinanceInfo.html

It looks like all of these are as of December 31, 2022, so it’s not as much of a lag as if it were June 30, 2022.

Yahoo Finance mirroring Bloomberg: Chicago Pension Debt Rises to $35 Billion as Mayor Hunts for Fix

Decades of chronic underfunding helped balloon Chicago’s pension liability, weighing on the city’s budget and credit ratings. Recent state-mandated contribution increases helped the city earn rating upgrades in the last year, including one from Moody’s Investors Service in November that allowed it to shed its one junk rating.

Johnson, who took office in May, has set up a pension working group that is charged with finding sustainable solutions to the long-term challenge.

Spokespeople for the city didn’t respond to a request for comment.

I bet they didn’t.

Their options are very constrained, due to past choices.

Mayor Johnson and the Chicago Pension Working Group

Let’s back up to when Chicago Mayor Johnson announced this pension working group for Chicago.

Official statement, 21 June 2023: Statement from Mayor Brandon Johnson on Pension Working Group

Today, my administration’s pension working group convened for the first time to address structural issues across the city’s four pension funds.

“I’m grateful to our pension working group for their willingness to work together to develop a sustainable path forward for the city’s pension funds.” said Mayor Brandon Johnson. “Today’s initial meeting included stakeholders representing my administration, the city council, the general assembly, organized labor and pension funds. Over the next several months, these individuals will work with a broader set of advisors from the financial and advocacy sectors to develop actionable solutions to meet the city’s obligations to retirees, workers, and taxpayers.”

The working group will form sub-groups to address specific pension issues and dedicated revenue as part of a comprehensive and balanced approach.

That’s the entirety of the statement, plus a listing of the group members:

- Kelly Burke, Illinois State Representative, 36th District

- Beniamino Capellupo, Senior Labor Advisor, City of Chicago

- John Catanzara Jr., President, Chicago Police Department Lodge 7

- Pat Cleary, President, Chicago Fire Fighters Union Local 2

- Pat Dowell, Alderman, 3rd Ward

- Jason Ervin, Alderman, 28th Ward

- Annette Guzman, Budget Director, City of Chicago

- Joe Healy, Secretary-Treasurer, Laborers’ District Council of Chicago

- Jeff Howard, Executive Vice President, SEIU Local 73

- Jill Jaworski, Chief Financial Officer, City of Chicago

- Andrea Kluger, Deputy Chief of Staff, Government Affairs, Chicago Federation of Labor

- Jason Lee, Senior Advisor, City of Chicago

- Robert Martwick, Illinois State Senator, 10th District

- Martha Merrill, Director of Research & Employee Benefits, AFSCME

- Cameron Mock

- Mike Rodriguez, Alderman, 22nd Ward & Chairman of City Council Workforce Development

- Steve Zahn

One can note the list: heavy on the public employee union representation, as well as other politicians.

Not seeing much in the way of representation of the people they’re probably expecting to pay for the pensions.

Though this is paywalled, I think the headline is enough — Greg Hinz at Crain’s: Biz groups excluded from Johnson’s pension panel

All that said, there are probably at least a couple on that list (oh, budget director, maybe even that Director of Research & Employee Benefits for AFSCME) who may remember why Chicago was forced to ramp up contributions to its pension funds recently.

The very short explanation: if they continued with their old contribution rates, the funds would have run out of assets, and be on a pay-as-they-go basis.

Before the Ramp-Up: Watching the Assets Go Away

In particular, MEABF (the municipal workers’ fund) was going to run out of assets by 2024.

STUMP has been around since 2014, so let’s check this out:

Nov 2014: Public Pension Watch: How Screwed is Chicago?

SPOILER ALERT: a lot.

Let me point out some language from a recent official report:

….

Having a negative impact on asset values was the need to liquidate investments to pay benefits on a monthly basis. In all, MEABF liquidated $496.3 million of investments to meet the Plan’s cash flow needs. [page 18]

…..

The Actuary projects that under the current funding policy, if all future assumptions are realized, the funding ratio is projected to deteriorate until assets are depleted within about 10 to 15 years. The current statutory funding mechanism impacts the ability to grow assets because in order to pay benefits, assets have and will continue to be liquidated.[page 20]….

Ah, the asset death spiral.

This is from the Comprehensive Annual Financial Report of the Municipal Employees’ Annuity and Benefit Fund of Chicago for the fiscal year ending December 31, 2013 (and 2012, but that’s an item I don’t want to touch right now.)

Let me explain the asset death spiral, which is when balance sheet weakness manifests itself in something really serious: a lack of cash flow to cover promised benefits.

Having to liquidate assets to cover cash flows is not necessarily a bad sign — if one has a decreasing liability (which means decreasing cash flow needs in the future).

This is not the case for Chicago. Nor Illinois.

One has to sell off assets when investment returns and pension contributions are too low to cover current cash flow needs. This reduces the asset amount for the pension funds…and if cash flow needs are increasing, you find that one has to liquidate more and more assets… until the fund is exhausted.

April 2017: Exactly How Screwed Are Chicago Pensions?

I’m glad you asked!

Very.

….

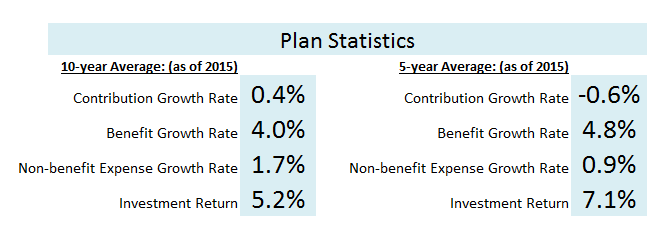

But, just to keep it simple, lets assume that today’s market is not a massive fed-induced bubble and that the MEABF is able to produce consistent 5.5% (their 15-year average) returns every year in perpetuity. Even then, the fund will only generate roughly $500mm per year in income compared to benefit payments growing to $1.3 billion…see the problem?

….

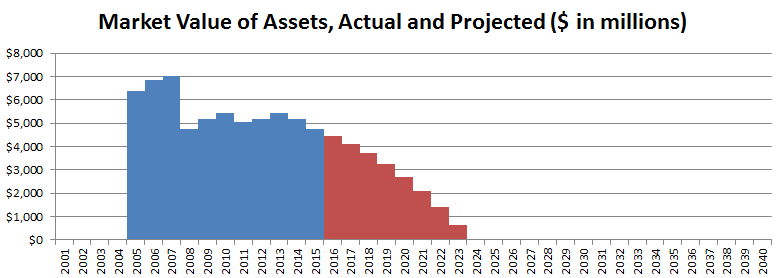

And, putting it all together, even if Chicago’s largest pension generates consistent positive returns for the foreseeable future, it will literally run out of cash in roughly 6 years.

May 2017: Testing to Death: Which Public Pensions are Cash Flow Vulnerable?

Note: that was before they ramped up the contributions.

But that gives you an idea why they had to ramp them up.

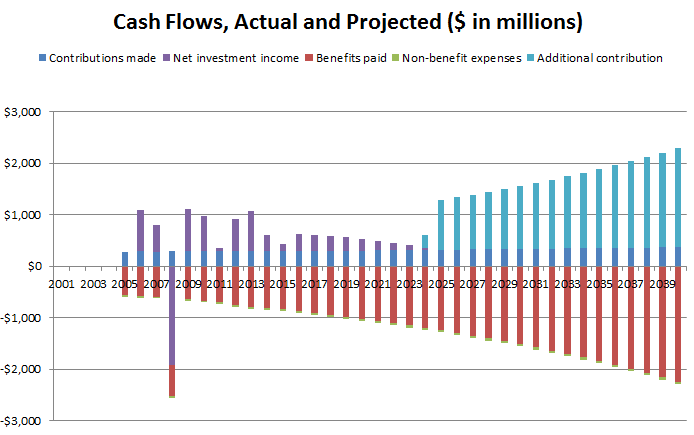

My baseline projection can be seen here in this April 2017 post: Watching the Money Run Out: A Simulation with a Chicago Pension

Current Trajectories are Barely Treading Water

That’s not the trajectory it’s on now, because they greatly increased contributions, as mentioned in the article.

The blue bars are what they actually paid, as a percentage of payroll, but the red bars are what they should have paid.

They’re still falling short.

This is what the funded ratio is doing, even with that large increase in contributions.

I could add the 2022 data points with the new reports, but it’s not like it helps.

The last time I tried a cash flow projection on the Chicago funds, they did not run out of assets, but that was assuming the contributions could grow as they are now. I don’t think they really can sustain that contribution growth. It is a strain on the city’s budget.

I suppose that contributions might be able to be cut a bit and the funds not go into an asset death spiral, but that’s a fine line to walk.

Few choices going forward

Given how this pension working group is constituted, obviously, benefit changes downward or increased contributions from workers are unlikely.

Reducing contributions, given current contributions are still inadequate, is a bad idea. The funded ratio is in asset death spiral territory, and very sensitive to adverse experience, whether markets or even retirees living a little longer.

Looking for additional revenue is really the only way they can go.

Brandon Johnson had been hoping to use his ideas for spending revenue on all sorts of new goodies in Chicago, but really, given that Chicago has the worst city pension situation in the U.S., he’s got to be spending any “excess” revenue on old services — that is, unfunded pension liabilities.

Way back in 2014, I wrote Public Pension Watch: Chicago, Not Waving But Drowning, and it is still true. This comes from decades of overpromising and underpaying for pensions.

Other cities and states also have underfunded pensions, but because they didn’t under-contribute or overpromise quite as badly as Chicago did, they have more options in dealing with their situations.

Not so Chicago.

I don’t envy this working group, and whatever business groups are still in Chicago, they should probably be happy they’re not touching any of this. There was slim chance of adjusting the benefit side of the equation, what with Brandon Johnson as a mayor, and unless they really had some fantastic revenue ideas, they were not likely to make headway.

Perhaps these labor folks will be pie-in-the-sky, believing ridiculous revenue projections and undervaluing of pensions, maybe they will fall for the “pensions don’t have to be funded!” crap coming from various groups. Maybe they will think pay-as-they-go will work just fine for the pension funds and not be scared of asset death spirals in the pension funds.

They should know that Illinois will not be forthcoming with funds for the city pension funds… the best they might do is get a little something for the teachers’ fund from the state. Illinois itself is under a crunch and is seeing revenue leave.

I am unsure how much power Chicago itself has in trying to impose or ask for taxes, as it is. We’ve already seen prior revenue-seeking deals (the parking meter one) go poorly. I see that Chicago Public Schools can impose tax hikes, but as I said, the above pension analysis is separate from CPS.

It will be interesting to see what comes out of this committee. I am not necessarily assuming they will be detached from reality until I actually see their work product. They may be very realistic as to likelihoods. Of course, perhaps their only purpose is to try to work deals with the Illinois state legislature. We shall see.

Related Posts

Public Pensions Watch: Sometimes Politicians Do the Right Thing

Nevada Pensions: Liability Trends

Happy Idea: Moving from Defined Benefit to "Defined Ambition"